Written by

Joshua Thompson

Joshua ThompsonArticle details

» 10 min read

This article covers information on Touchstone Exploration.

LON:TXPPositive #1 – Oil & Gas friendly country

Touchstone Exploration’s operations in Trinidad and Tobago benefit from the country’s longstanding support for the oil and gas industry. The nation boasts a well-established regulatory framework, a skilled workforce, and extensive infrastructure catering to energy projects. This stable environment has historically attracted and sustained energy investments.

Recent political developments further underscore this supportive landscape. On 16 March 2025, Stuart Young, the current Minister of Energy and Energy Industries, is set to assume the role of Prime Minister, succeeding Keith Rowley. Young’s tenure as Energy Minister since April 2021 has been marked by a series of reforms aimed at revitalising the sector. His elevation to Prime Minister suggests a continued commitment to fostering a conducive environment for oil and gas operations.

A big positive is the Touchstone management team appears to have an excellent relationship with the government, which should enable future negotiations.

One specific area where further reform could significantly benefit companies like Touchstone is the renegotiation of fixed-price gas contracts. Something we will cover a little later.

Negative #1 – Cascadura – Not quite the asset anticipated?

Steeper Decline Rates

Following its commissioning in September 2023, the Cascadura field experienced natural declines in production. Cascadura’s production is following a turbidite decline curve, meaning initial high flow rates have tapered off more quickly than anticipated.

In the first quarter of 2024, average production decreased by 18% to 7,015 barrels of oil equivalent per day (boe/d) from 8,504 boe/d in the fourth quarter of 2023, primarily reflecting natural declines from the Cascadura field.

Drilling and Infrastructure Delays

The Cascadura structure has proven more intricate than initially anticipated. During testing of the Cascadura-3ST1 well, initial promising oil flows were followed by the unexpected production of formation water, mud, and sand, indicating a breach into a lower water-bearing sand.

Gas Processing Constraints

Infrastructure limitations, including delays in optimising the gas processing facilities, have impacted Cascadura’s full production potential. While expansions have been implemented to increase processing capacity, the ramp-up has been slower than anticipated, affecting overall output.

Positive #2 – Basic Valuation

As of writing this article, TXP is valued at £0.22/share and a total market cap of £52.02 million. I believe the valuation in the recent Shore Capital note of 36p is fair – this represents a 38.9% discount to the estimated share value.

A quick NAV approach would be:

- 2P Reserves: 67.4 million barrels of oil equivalent (boe).

- Enterprise Value (EV): £81.3 million.

- Net Debt: £21.6 million

- EV/boe (2P): £1.21 per boe.

- Shares in Issue: 236.46 million.

| EV/boe Multiple | Implied EV (£M) | Implied Share Price (p) |

|---|---|---|

| £1.21/boe (Current) | £81.3M | 25.3p |

| £1.50/boe | £101.1M | 33p |

| £2.00/boe (Peer Avg.) | £134.8M | 47.8p |

| £2.50/boe | £168.5M | 63p |

Negative #2 – Is the Management delivering?

The erosion of shareholder value of the recent years would give a simple answer – no.

One of the ongoing concerns with Touchstone Exploration (TXP) is whether its leadership team has truly learned from past mistakes. While the company is generating positive free cash flow (FCF), investors – particularly institutional investors (IIs) are likely questioning whether that cash will be allocated effectively. The post-Cascadura discovery strategy appeared overly aggressive and, at times, lacked the structured decision-making process expected from a company of this size.

- Some of Touchstone’s past strategic choices seemed driven more by optimism and gut feeling rather than rigorous analysis and risk assessment.

- The company has a track record of making decisions that, in hindsight, appear rushed or based on overly optimistic assumptions. This has eroded confidence among long-term shareholders.

- Institutional investors may still be wary of whether TXP’s leadership has the discipline to allocate capital responsibly rather than pursuing high-risk projects without proper due diligence.

The Trinity Fiasco – A Failed Acquisition Attempt

Initial Offer

On 1 May 2024, Touchstone announced an all-share offer to acquire Trinity, valuing each Trinity share at approximately 61.9 pence, based on Touchstone’s closing share price of 41.25 pence on 30 April 2024. This valued Trinity’s entire issued share capital at around £24.1 million. The acquisition aimed to consolidate onshore oil and gas operations and enhance Touchstone’s market position in Trinidad.

LOL Bid

The acquisition process took an unexpected turn on 2 August 2024, when Lease Operators Limited (LOL) made a recommended cash offer for Trinity at 68.05 pence per share, valuing the company at approximately £26.4 million. This offer provided a significant premium and immediate cash value, making it more attractive to Trinity shareholders compared to Touchstone’s stock-based proposal.

Withdrawal of Support and Collapse of Touchstone’s Offer

In light of LOL’s superior offer, the Trinity Board withdrew its recommendation for Touchstone’s offer and postponed the related court sanction hearing indefinitely. Despite having received irrevocable undertakings from shareholders representing approximately 38.9% of Trinity’s ordinary share capital, these commitments lapsed following the board’s withdrawal of support. Consequently, Touchstone’s offer collapsed, leading to the termination of the acquisition attempt.

The Impact

- Legal Fees – I couldn’t find any data on the legal fees, however we can assume that these will have been substantial.

- Wasted Energy – The company expended considerable time and resources negotiating the acquisition, diverting attention from other strategic initiatives.

- Trinity Losses – Trinity reported gross tax losses carried forward totalling $224.4 million, comprising $34.7 million in the UK and $189.7 million in Trinidad and Tobago.

The Board Size & Directors Renumeration

In 2023, Touchstone’s President and Chief Executive Officer, Paul Baay, received total compensation of approximately $744,610, comprising 48.9% salary and 51.1% bonuses, including company stock and options. This does seem excessive for an underperforming company.

As of the 2024 Annual General Meeting, Touchstone’s Board consisted of nine members, including eight independent, non-management directors and the President and Chief Executive Officer. Questions were raised about the need for such a large board and their direct impact on the performance of the business. However this seems to have fallen on deaf ears as there is no update as of March 2025.

Positive #3 – Central Block Acquisition

My belief is that this is the single biggest investment case for Touchstone.

Touchstone Exploration’s agreement to acquire Shell Trinidad Central Block Limited (STCBL) represents a pivotal move to enhance its production capacity and market reach. The acquisition, valued at $23 million, is expected to close in the second quarter of 2025, pending regulatory approvals.

Immediate Production Growth: The Central Block currently produces approximately 18 million cubic feet per day (MMcf/d) of natural gas and 200 barrels per day of natural gas liquids, equating to about 3,200 barrels of oil equivalent per day (boe/d). This acquisition is projected to increase Touchstone’s net production by approximately 2,080 boe/d, marking a significant boost in near-term output.

Access to Global LNG Pricing: STCBL holds gas marketing contracts that provide access to both the domestic market and the Atlantic LNG facility. This dual access enables Touchstone to tap into global LNG markets, where prices are notably higher, potentially leading to improved margins and accelerated cash flow growth.

Operational Synergies: The Central Block’s infrastructure, including an 80 MMcf/d gas processing plant and existing pipelines, aligns seamlessly with Touchstone’s current assets. This integration facilitates efficient monetisation and supports future expansion plans.

Reconfiguration: In early 2025, the compressors at the Evergreen Facility underwent reconfiguration to help processing capabilities. It is currently unknown how this new configuration has gone.

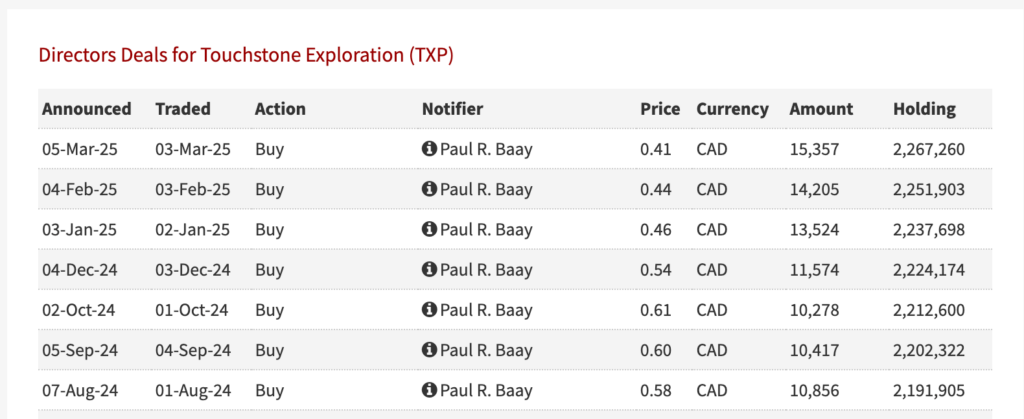

Negative #3 – Insider Open Market Share Purchases

It’s disappointing to see the directorship not purchasing shares in the open market. With such high renumeration, it would go a long way for weary shareholders to see open market purchases.

Employee Share Purchase Plan (ESPP) or bonus-related awards. Not open market purchases.

Positive #4 – A Community

One of the things I learned from the Gamestop fiasco was the power of the community when a share price moves (in either direction). Make no mistake – having over 13% of shareholding in one place goes a long way when it comes to moving a small cap.

The Discord Community

The Touchstone Exploration Discord has just shy of 1000 members which you can join. In the Discord you’ll find some extremely intelligent people – with many having a background in Oil & Gas. Many shareholders will posts their buys and sells as well as live commentary around news events.

Touchstone GPT

A ChatGPT with all of the RNS’s stored in it’s memory has been created for new investors to easily access information and ask questions about the company to do some quick research. This can be useful as part of a diligent investor doing their due diligence.

Positive #5 – Renegotiation of Gas Prices

Recent policy changes in Trinidad and Tobago have opened avenues for third-party gas producers to access international Liquefied Natural Gas (LNG) markets through facilities operated by major players like Shell and BP. LNG prices in these markets are significantly higher, estimated at approximately $7.50 per Mcf. By leveraging these developments, Touchstone aims to diversify its sales channels and capitalise on more lucrative pricing structures.

Access to Global LNG Markets

Securing higher gas prices could substantially boost Touchstone’s revenues. Estimates suggest that aligning sales with global LNG pricing could unlock an additional $40 to $50 million in revenue. This influx would not only enhance cash flow but also fund continuous drilling programs, supporting the company’s aggressive expansion strategy.

Financial Implications

Securing higher gas prices could substantially boost Touchstone’s revenues. Estimates suggest that aligning sales with global LNG pricing could unlock an additional $40 to $50 million in revenue. This influx would not only enhance cash flow but also fund continuous drilling programs, supporting the company’s aggressive expansion strategy.

Can they get it done?

I can’t imagine a renegotiation of gas pricing in Trinidad is going to be easy. It remains to be seen whether the management have the ability to get this one over the line.

Positive #6 – Land Acreage

Touchstone Exploration has a significant land acreage position in Trinidad, with a total of 144,893 net acres under its control. This extensive acreage provides the company with strong development and exploration opportunities, particularly in the Herrera fairway, where it has secured multiple high-potential blocks.

Key Acreage Highlights

Rio Claro Block: 31,983 acres (25,586 net), 80% working interest.

Cipero Block: 29,924 gross acres, 80% working interest.

Charuma Block: 72,784 gross acres, 80% working interest.

Balata East & Deep Horizons: 28,000 acres acquired through an asset swap.

Cretaceous Targets

Identified Anomalies:

Multiple Cretaceous anomalies detected in exploration blocks. These could open up significant new opportunities for onshore hydrocarbon production.

Depth of Targets:

a) Cocos Prospect: ~7,000 feet.

b) St. Croix Prospect: ~13,000 feet.

c) Kraken Prospect: ~15,000 feet.

Historical Drilling Data:

1994: Exxon’s IGR-1 well drilled to 12,762 feet, encountering residual oils in sandstones and carbonates.

1995: Exxon’s SCRX-1 well drilled to 17,587 feet, finding residual oil in sandstones.

2005: Talisman’s Zaboca-1 well drilled to 15,681 feet, but it did not encounter sandstones.

Cipero Block Exploration:

The block has Herrera and Cretaceous targets identified. Drilling is expected after a minimum three-year preparation period.

TLDR (Too Long Didn’t Read)

| 🔥 Key Topic | 📈 Summary |

|---|---|

| 📍 Pivotal Year for TXP | 2025 is a crucial year for Touchstone Exploration, with the market demanding execution and results. |

| 🌍 Positive #1 – Oil & Gas Friendly Country | Trinidad’s government remains supportive of oil and gas. Stuart Young’s appointment as PM could bring further energy sector reforms. |

| ⛽ Negative #1 – Cascadura Challenges | Production rates have declined faster than expected, drilling delays persist, and gas processing constraints impact output. |

| 💰 Positive #2 – Basic Valuation | TXP currently trades at a 38.9% discount to its estimated fair value (36p target). Peer comparisons suggest significant upside potential. |

| ⚠️ Negative #2 – Management Performance | TXP’s leadership has made aggressive and sometimes questionable decisions post-Cascadura, leading to skepticism among investors. |

| 🛑 Trinity Takeover Failure | TXP’s failed bid for Trinity (outbid by Lease Operators Limited) wasted resources and lost potential tax advantages ($224.4M in carryforward losses). |

| 🏛️ Negative #3 – Board Size & Remuneration | CEO Paul Baay’s $744,610 salary is seen as excessive given the company’s underperformance. The board size raises efficiency concerns. |

| 📢 Positive #3 – Central Block Acquisition | The $23M acquisition could be TXP’s biggest growth driver, adding production, LNG access, and strategic synergies. |

| 🔧 Central Block Reconfiguration | Compressor rework at the processing plant delayed production; final adjustment costs remain unknown. |

| 📉 Negative #4 – Lack of Insider Buys | Despite high salaries, directors have not made open market share purchases, raising investor concerns. |

| 👥 Positive #4 – A Strong Shareholder Community | Over 13% of shares are held within a coordinated investor community, with a thriving Discord group. |

| 💸 Positive #5 – Gas Price Renegotiation | TXP aims to secure higher LNG-linked prices (from $2.30/Mcf to ~$7.50/Mcf), unlocking up to $50M in additional revenue. |

| 🧐 Can They Get the New Gas Prices? | The renegotiation process won’t be easy; management’s ability to execute remains uncertain. |

| 🌎 Positive #6 – Land Acreage | Potential for drilling some very interesting targets! |

Last updated

Category

InvestingLikes

More posts

You might also enjoy

Investing

UK Pension Giants Explore £1bn Scale-up Fund

UK pension providers are exploring a £1bn-plus scale-up fund, although its manager, commitments, fees and launch date remain undisclosed.

JoshuaJuly 27, 2026

Investing

Burnham actively considers scrapping council tax and stamp duty. What impact does this have on UK BTL Investors?

The Government is reportedly considering property tax reform, including Fairer Share’s Proportional Property Tax. We examine the potential costs, risks and planning implications for buy-to-let investors.

JoshuaJuly 27, 2026

Investing

Cambridge Cognition revenue rises 16% as debt is cleared

Cambridge Cognition grew H1 revenue by 16%, improved its adjusted EBITDA loss and cleared its borrowings after a £2.5 million placing.

JoshuaJuly 27, 2026

Star Rating

No ratings yet

Comments

No comments yet - start the conversation.